The global memory market is in structural collapse. Since early 2024, a deliberate shift in manufacturing priority has redirected the world’s semiconductor capacity toward AI infrastructure, triggering what analysts and vendors alike are calling “RAMmageddon” — a shortage so severe that Dell’s COO Jeff Clarke stated the company “has never witnessed costs escalating at the current pace.” This is not a temporary supply blip. It is a fundamental restructuring of who gets memory and at what price. This tutorial walks you through exactly what is happening, why SK Hynix’s planned $10–14 billion U.S. IPO matters, and — most importantly — how to protect your hardware budgets, AI deployments, and procurement strategy right now.

What This Is

The Structural Shift Behind RAMmageddon

According to the NotebookLM research report compiled from multiple industry sources, “RAMmageddon” is not a supply chain disruption in the traditional sense. It is the direct consequence of AI infrastructure demands overwhelming a memory manufacturing ecosystem that was never designed to serve two masters simultaneously.

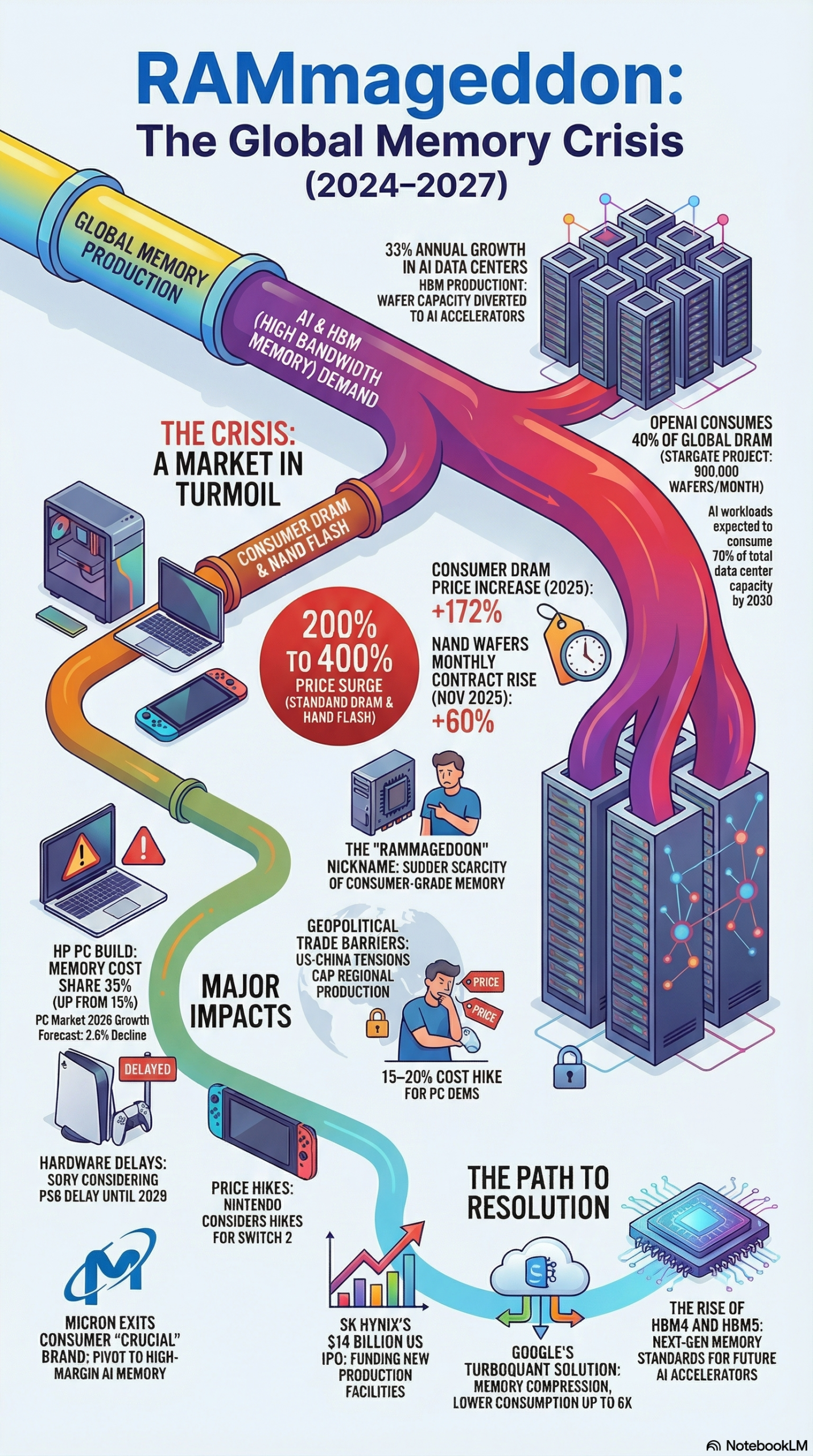

Here is the core mechanism: High Bandwidth Memory (HBM) — the specialized memory stacked inside NVIDIA GPUs, Google TPUs, and other AI accelerators — requires dramatically more wafer fabrication capacity per bit than conventional DDR4 or DDR5. When AI infrastructure spending exploded in 2023 and 2024, the three dominant memory producers — Samsung Electronics, SK Hynix, and Micron Technology — did the rational business thing and shifted their most advanced fabs toward HBM production. The casualty was consumer and enterprise DRAM.

The scale of this reallocation is staggering. OpenAI’s “Stargate Project” requires approximately 900,000 wafers per month and is projected to consume up to 40% of the global DRAM supply. OpenAI has bypassed distributors entirely, forming direct partnerships with Samsung and SK Hynix to secure undiced wafers straight from the fab. That is not a customer buying product — that is a customer buying factory output.

Samsung has responded by expanding its 1c DRAM capacity to 60,000 wafers per month, specifically allocated for HBM4 production. Micron has gone further: it has scrapped the entire “Crucial” consumer brand and pivoted entirely to high-margin AI and enterprise memory. Its HBM4 roadmap targets a 12-layer stack with 36GB capacity. These are not short-term pivots. These are permanent strategic repositions.

SK Hynix’s role in this ecosystem is particularly pivotal. Currently trading on South Korea’s KOSPI exchange, SK Hynix has filed for a U.S. IPO targeting $10–14 billion in proceeds. According to TechCrunch reporting from March 27, 2026, this listing is designed to fund the additional production capacity needed to eventually alleviate the shortage. The company has already committed $7.9 billion to acquire ASML EUV scanners — the lithography machines required to fabricate the next generation of memory at scale. Justin Kim, President and Head of AI Infra at SK Hynix, has described HBM4 as “a symbolic turning point beyond the AI infrastructure limitations” and “a core product for overcoming technological challenges.”

The next-generation HBM4 standard itself represents a technical leap: it doubles the interface width from 1,024-bit to 2,048-bit and incorporates a base die fabricated on 5nm and 4nm logic nodes — a “logic-in-memory” architecture that begins blurring the line between memory and processor. Samsung’s implementation targets 13 Gbps speeds using its 4nm process for the base die.

The shortage is, in other words, a product of success: AI has grown so fast that it is consuming the memory supply faster than the industry can build new fabs.

Why It Matters

The Real Cost to Practitioners, Buyers, and Builders

If you buy hardware, build AI systems, or manage technology infrastructure, this crisis is already affecting your budget. Here is what the data shows.

For enterprise IT and procurement teams, the most immediate impact is price. Standard DRAM prices rose by 172% throughout 2025 alone. DDR5 module prices have more than doubled in markets like Tokyo’s Akihabara district. The Team Group GM stated in November 2025: “The RAM pricing crisis has only just started… [the] problem will get worse in 2026 as DRAM and NAND prices double in one month.” Enterprise hardware lead times have already extended into 2027 for some configurations.

For PC OEMs and their customers, the math is brutal. HP Inc. has disclosed that memory now accounts for 35% of PC build materials — up from 15–18% historically. That is more than double. Gartner analysts predict that laptops priced under $500 will become financially unviable by 2027–2028. Entry-level consumer laptops are being priced out of existence. Lenovo disclosed that its memory inventories are running 50% above normal levels as a deliberate hedge against further price hikes — a strategy that adds carrying cost but protects against margin collapse.

For AI engineers and ML practitioners, the shortage directly constrains what you can run locally and what you can afford to run in the cloud. GPU memory availability is tighter, and the cost of memory-intensive inference workloads is rising. NVIDIA has shifted toward LPDDR memory in some AI products, creating new pressure on a memory type previously reserved for premium mobile devices.

For consumer electronics makers, the collateral damage is visible: Sony is reportedly considering delaying the PlayStation 6 until 2029 due to component costs, and Nintendo may raise the price of the Switch 2 to protect margins.

Geopolitically, the crisis has a compounding layer. In 2025, Samsung and SK Hynix halted sales of older semiconductor manufacturing equipment to Chinese entities to avoid U.S. regulatory backlash. U.S. Commerce Secretary Howard Lutnick has signaled that non-U.S.-investing chipmakers could face tariffs of up to 100%. Apple has already responded by accelerating plans to source all U.S.-bound iPhones from India. The supply chain is fracturing along geopolitical lines at exactly the moment it needs to be scaling.

The Data

Memory Market Impact Summary: Key Figures and Manufacturer Responses

| Entity | Impact / Response | Source |

|---|---|---|

| Samsung Electronics | Expanded 1c DRAM capacity to 60,000 wafers/month for HBM4; using 4nm process nodes | Research Report |

| SK Hynix | Filed $10–14B U.S. IPO; committed $7.9B for ASML EUV scanners | TechCrunch |

| Micron Technology | Scrapped “Crucial” consumer brand; pivoting to 12-layer HBM4 with 36GB capacity | Research Report |

| OpenAI (Stargate) | ~900,000 wafers/month required; projected to consume 40% of global DRAM output | Research Report |

| Dell Technologies | Costs escalating at “unprecedented” pace; stock downgraded by Morgan Stanley | Research Report |

| HP Inc. | Memory = 35% of PC build materials (was 15–18%) | Research Report |

| Lenovo | Carrying 50% above-normal memory inventory as price hedge | Research Report |

| Sony | Reportedly considering PS6 delay to 2029 | Research Report |

| Gartner | Sub-$500 laptops financially unviable by 2027–2028 | Research Report |

| DRAM prices (2025) | Rose 172% throughout 2025; retail DDR5 prices more than doubled | Research Report |

HBM Generation Comparison

| Spec | HBM3 | HBM4 |

|---|---|---|

| Interface width | 1,024-bit | 2,048-bit |

| Base die process | Standard logic | 5nm / 4nm logic |

| Architecture approach | Memory-only stack | Logic-in-memory |

| Target speed (Samsung) | ~8 Gbps | 13 Gbps |

| Micron stack layers | 8-layer | 12-layer |

| Micron max capacity | ~24GB | 36GB |

Step-by-Step Tutorial

How to Build a RAMmageddon-Resilient Technology Strategy

This is a practitioner’s playbook. Whether you are a startup CTO, an enterprise IT director, an AI engineer building production systems, or a procurement lead trying to hold margin — these are the concrete steps you need to take right now.

Phase 1: Audit Your Current Memory Exposure

Step 1: Inventory all memory-dependent hardware in your pipeline.

This means every server refresh, workstation procurement, and GPU upgrade you have planned for 2026 and 2027. Pull the bill of materials for each. Note the memory type (DDR4, DDR5, LPDDR5, HBM) and the quantity. You need to know your total exposed volume.

If you are running cloud infrastructure, pull your memory-intensive instance types. AWS r-series, Google Cloud m-series, and Azure memory-optimized VMs have all seen cost increases that are being passed through to customers. Your cloud bill is also a memory bill.

Step 2: Classify your memory needs by urgency and replaceability.

Tier your requirements:

– Tier 1 (Critical, time-sensitive): Production AI inference servers, data pipeline machines, and any hardware with a firm launch deadline.

– Tier 2 (Important, flexible): Developer workstations, staging environments, planned upgrades that can be deferred 6–12 months.

– Tier 3 (Nice-to-have): Exploratory hardware, lab equipment, dev/test environments that can run lean configurations.

This tiering will determine your procurement urgency and the degree of architectural optimization you need in each category.

Phase 2: Lock In Supply With Long-Term Agreements

Step 3: Contact your primary hardware vendors about long-term supply agreements (LTAs).

The research report is explicit that smaller firms should anticipate “hourly pricing” models and requirements for three-year cash payments upfront from some foundries. You do not have the leverage of a hyperscaler, but you do have the ability to commit to volume over time. Most major distributors — including Arrow, Avnet, and TD Synnex — offer LTA programs that lock pricing for 12–24 months in exchange for volume commitments.

Get those conversations started now. Every week you delay is a week the price floor rises further.

Step 4: Diversify your supplier base.

If your memory supply chain runs through a single distributor, you are exposed. The shortage is creating allocation queues, and distributors are prioritizing their largest customers. Open accounts with at least two or three certified distributors and get on their allocation lists. For enterprise DRAM specifically, also look at direct OEM supply programs (Dell EMC, HPE, Lenovo) that bundle memory into server contracts — these often provide better allocation than spot market purchases.

Phase 3: Implement Software-Based Memory Optimization

Step 5: Evaluate Google TurboQuant for AI workloads.

This is one of the most important tactical moves available to AI practitioners right now. Google’s TurboQuant is an ultra-efficient AI memory compression technology that claims to reduce memory consumption by 6x. The research report documents that it has demonstrated the ability to run a 9-billion-parameter model with a 20,000-token context window on a standard 16GB MacBook Air. That is a workload that would normally require 48–64GB of memory.

To evaluate TurboQuant for your workloads:

1. Identify your heaviest inference models by parameter count and context window requirement.

2. Run a benchmark of your current memory utilization at peak load using nvidia-smi (for GPU) or system profilers.

3. Test quantized versions of your models (INT8, INT4, or FP8 depending on your framework) against your accuracy benchmarks.

4. Compare memory footprint before and after quantization. Even conservative 2–3x compression dramatically expands what you can run on existing hardware.

Step 6: Adopt memory-efficient model architectures.

Beyond quantization, architectural choices matter. For practitioners building or selecting AI models:

- Prefer models with efficient attention mechanisms: Linear attention variants (e.g., Mamba, RWKV) consume far less memory than standard transformer attention for long contexts.

- Use gradient checkpointing in training: This trades compute time for memory — acceptable when memory is the constraint.

- Implement KV-cache optimization: For LLM inference, the KV cache is often your largest memory consumer. Techniques like grouped query attention (GQA) and multi-query attention (MQA) reduce cache size significantly.

- Right-size your context windows: If your production use case only needs 4,096 tokens of context, do not deploy a model configured for 128K context. Every token of unnecessary context window burns memory at inference time.

Phase 4: Redesign Hardware Procurement for the New Reality

Step 7: Shift toward memory-efficient compute configurations.

With HP reporting that memory now accounts for 35% of PC build materials, the ROI calculation on “buying more RAM” has changed fundamentally. Before automatically specifying maximum memory, ask whether the workload actually needs it. In many cases, a well-optimized software stack on a leaner memory configuration outperforms a poorly optimized stack on a high-memory machine — and costs significantly less.

Specific hardware strategies:

– For AI inference servers: Prioritize GPU memory bandwidth (HBM3/HBM4 equipped GPUs) over raw capacity. A faster, smaller memory bus often outperforms a larger, slower one for inference throughput.

– For developer workstations: Consider whether LPDDR5 ultrabooks (48GB configurations are now available on some platforms) can replace DDR5 desktops for your developers’ actual workflows.

– For data center: Evaluate CXL (Compute Express Link) memory expansion as a way to pool memory across nodes, reducing per-server memory requirements.

Step 8: Build a rolling procurement schedule.

One of the key insights from the research report is that Lenovo is carrying 50% above-normal memory inventory as a deliberate hedge. You do not need to go that far, but you should build a 3–6 month rolling buffer for your most critical memory SKUs. Set procurement calendar reminders and buy incrementally rather than waiting for a hardware refresh cycle to force a panic purchase.

Phase 5: Monitor the Market for Relief Signals

Step 9: Track the SK Hynix U.S. IPO process.

The TechCrunch reporting frames SK Hynix’s $10–14 billion U.S. IPO as a “critical attempt to close the valuation gap between Korean and U.S. chipmakers” and as the primary near-term mechanism for funding the capacity expansion needed to end RAMmageddon. If the IPO succeeds and raises near its target, capital flows into new fab construction. That takes 18–36 months to translate into shipping product, but the market will price relief in advance.

Watch these signals:

– SK Hynix U.S. IPO filing progress (S-1 registration, SEC approval timeline)

– ASML EUV scanner delivery confirmations (SK Hynix’s $7.9B order is a leading indicator of future capacity)

– Quarterly earnings guidance from Samsung, Micron, and SK Hynix on HBM vs. DRAM allocation

– DRAM spot prices on DRAMeXchange — a sustained 3-month decline signals real supply improvement

Step 10: Validate your geopolitical exposure.

If any part of your supply chain sources components that touch U.S.–China trade restrictions, run a dependency audit now. U.S. Commerce Secretary Howard Lutnick’s signals about 100% tariffs on non-U.S.-investing chipmakers represent a potential escalation that could further disrupt supply. The Apple-to-India pivot is the model: identify your exposure and start the diversification process before you are forced into it under pressure.

Expected Outcome: Following this 10-step process gives you a defensible position against continued price increases, supply constraints through 2027, and geopolitical disruptions. You will not eliminate the impact of RAMmageddon, but you will stop being surprised by it.

Real-World Use Cases

How Different Teams Are Applying These Strategies Today

Use Case 1: AI Startup Cutting Inference Costs With Quantization

Scenario: A 20-person AI startup running production LLM inference on rented A100 GPU instances is seeing cloud costs climb 30% quarter-over-quarter as memory-intensive workloads drive up instance pricing.

Implementation: The engineering team audits their model deployment configurations and discovers they are running full FP32 inference on a 7B-parameter model. They implement INT8 quantization using their framework’s built-in quantization tooling, cutting memory usage roughly in half. This allows them to shift from 80GB A100 instances to 40GB A100 instances for the same throughput. They apply TurboQuant-style compression techniques for their longest-context requests.

Expected Outcome: 40–50% reduction in GPU instance costs for inference workloads. The accuracy delta from INT8 quantization is within acceptable bounds for their use case (less than 1% degradation on their benchmark suite). The team redeploys the savings into development compute.

Use Case 2: Enterprise IT Director Locking In Hardware Pricing

Scenario: An IT director at a mid-size financial services firm has a server refresh cycle planned for Q3 2026, covering 200 application servers with DDR5 DRAM requirements.

Implementation: Rather than waiting for the refresh cycle to trigger spot-market procurement, the director negotiates a long-term supply agreement with their primary hardware OEM in Q1 2026, committing to a 12-month purchase schedule at locked pricing. They tier their server specifications: Tier 1 production servers get full memory configurations; Tier 2 dev/test servers are spec’d at 50% of normal RAM with CXL memory expansion ports for future scaling.

Expected Outcome: Based on the 172% DRAM price increase documented in 2025, the LTA pricing represents a projected savings of $180,000–$220,000 over spot-market procurement across the refresh cycle. The tiered specification approach reduces upfront capital outlay by 25%.

Use Case 3: Consumer Electronics Product Manager Reassessing Launch Plans

Scenario: A product manager at a mid-tier laptop brand is planning a new consumer laptop line targeting the $399–$499 price point for a 2027 launch.

Implementation: The PM runs a cost modeling exercise using current memory pricing trends. Based on HP’s disclosure that memory now represents 35% of PC build materials and Gartner’s prediction that sub-$500 laptops become financially unviable by 2027–2028, the analysis shows the target price point is unachievable with standard memory configurations. The team pivots: they redesign the SKU around LPDDR5 (more efficient, though still expensive) with 8GB configurations and position the product differently as a Chromebook-adjacent “cloud-first” device rather than a general-purpose laptop.

Expected Outcome: The repositioned product is viable at the target price point and actually aligns better with the team’s target buyer (students, light users). The memory footprint is cut by 40% versus the original spec. The trade-off is clear messaging about the device’s intended use case.

Use Case 4: Procurement Team Building a Geopolitical Supply Hedge

Scenario: A global tech company sources components through a supply chain with significant exposure to U.S.–China trade policy. Their memory procurement runs through distributors whose allocations depend partly on Chinese fab output.

Implementation: Following the model of Apple’s pivot to India and the documented halting of equipment sales to Chinese entities by Samsung and SK Hynix, the procurement team maps every memory SKU to its country-of-origin fab. They identify the SKUs with highest geopolitical risk and begin qualifying alternative sources from Korean and U.S.-aligned fabs. They build a 90-day buffer stock for the five highest-risk SKUs.

Expected Outcome: The company reduces its geopolitical exposure on critical memory components by 60% within two quarters. The buffer stock program adds 8% to carrying costs but eliminates production halt risk from a tariff escalation event.

Common Pitfalls

Mistakes That Will Cost You During RAMmageddon

Pitfall 1: Waiting for prices to normalize before buying.

Many procurement teams are holding off on memory purchases expecting the market to correct. Based on the Team Group GM’s November 2025 warning and the structural nature of the supply shift, waiting is the wrong call. The capacity needed to end this shortage — including SK Hynix’s new fabs funded by the U.S. IPO — takes 18–36 months to come online after investment is committed. Prices are more likely to continue rising in 2026 than to fall. Buy what you need now and lock in pricing where possible.

Pitfall 2: Over-specifying memory on non-critical hardware.

With memory prices 172% higher than 2024 levels, over-provisioning RAM on developer workstations, staging servers, and test environments is a direct hit to budget that delivers no corresponding performance benefit. Audit your non-production specs and right-size aggressively.

Pitfall 3: Ignoring software-level memory optimization.

The hardware shortage is partially addressable through software. Not evaluating quantization, compression, and memory-efficient architectures for AI workloads is leaving significant efficiency gains on the table. Google TurboQuant’s 6x compression claim is the headline example — even conservative implementations can dramatically reduce memory requirements for inference.

Pitfall 4: Single-source procurement.

With allocation queues forming at distributors, depending on a single vendor is a production risk. Qualify at least two suppliers for every critical memory SKU before you need them, not after.

Pitfall 5: Ignoring the geopolitical layer.

Treating the memory shortage as a pure supply-demand issue misses the geopolitical dimension. U.S. tariff signals toward non-U.S.-investing chipmakers and the documented equipment sales halts to China represent real supply chain disruption risks that procurement teams must model explicitly.

Expert Tips

Pro-Level Moves for Advanced Practitioners

Tip 1: Use DRAM spot price indices as a leading indicator. Track DRAMeXchange and TrendForce’s monthly DRAM contract price reports. A 10–15% spot price decline sustained over two quarters usually precedes contract price relief by 3–6 months. This gives you a signal to time any deferred purchases.

Tip 2: Negotiate memory upgrades into server contracts now, not later. When buying servers, negotiate a right-to-upgrade memory within 12–18 months at contracted pricing. OEMs are more willing to offer this during purchase negotiations than after. This gives you flex capacity without the spot-market exposure.

Tip 3: Evaluate CXL memory pooling for data center workloads. Compute Express Link (CXL) 2.0 enables memory pooling across servers, letting you efficiently share a large memory pool rather than over-provisioning each node individually. For memory-intensive but bursty workloads — like ML model loading or large in-memory databases — this architecture significantly improves memory utilization.

Tip 4: Monitor SK Hynix’s S-1 filing when it publishes. The S-1 registration statement for SK Hynix’s U.S. IPO will contain detailed financial disclosures about production capacity, capital expenditure plans, and HBM vs. DRAM allocation. This is some of the most detailed public data on future memory supply timelines you will find anywhere. Read it carefully.

Tip 5: Build memory efficiency into your procurement criteria. When evaluating AI accelerator purchases, include GB/W (gigabytes per watt) and memory bandwidth efficiency in your scoring criteria — not just raw capacity. As the HBM4 standard evolution shows, the industry is moving toward higher-efficiency, higher-bandwidth memory rather than simply more gigabytes. Hardware that leverages this trend will remain viable longer.

FAQ

Questions Practitioners Are Actually Asking

Q1: When will the memory shortage end?

There is no reliable short-term end date. The research report indicates that enterprise hardware lead times have already extended into 2027, and the Team Group GM warned in November 2025 that prices would continue rising in 2026. The most credible relief pathway is SK Hynix’s U.S. IPO funding new fabs — but new semiconductor fab construction takes 18–36 months to produce output after groundbreaking. A meaningful supply correction before late 2027 or 2028 is unlikely based on current trajectories.

Q2: Should I switch from DDR5 to LPDDR5 for my workstations to save money?

Potentially yes, but the tradeoff is nuanced. LPDDR5 is more power-efficient and is increasingly available in higher capacities (48GB on some laptop platforms), but it is soldered to the motherboard on most implementations — meaning no future upgrade path. If your use case is stable and you are comfortable with the fixed memory ceiling, LPDDR5-based systems can offer cost advantages. If workload memory requirements might grow, the inability to upgrade is a real constraint.

Q3: Is Google TurboQuant production-ready?

Based on documented research, TurboQuant has demonstrated production-relevant results — specifically running a 9B-parameter model with a 20,000-token context window on a 16GB MacBook Air. Whether it is suitable for your specific production workload depends on your accuracy requirements and the characteristics of your models. It is worth running your benchmark suite against TurboQuant-compressed models before deploying to production.

Q4: How does the SK Hynix U.S. IPO actually help with the shortage?

The IPO is a capital raise mechanism. The $10–14 billion target, combined with SK Hynix’s existing $7.9 billion ASML EUV scanner commitment, funds the construction of new leading-edge fab capacity. More capacity means more wafer output, which eventually translates to more DRAM supply. Additionally, a successful listing at scale signals to other Korean and global chipmakers that U.S. equity markets are viable for funding expansion, potentially encouraging parallel capital raises that accelerate the industry’s total capacity growth.

Q5: What should an AI engineer prioritize right now to reduce memory dependency?

Three things in priority order: First, quantize your inference workloads — INT8 or FP8 quantization typically delivers 2–4x memory reduction with acceptable accuracy tradeoffs for most production use cases. Second, optimize your KV cache — for LLM inference, KV cache management (GQA, MQA, cache eviction policies) is the highest-leverage memory optimization available without architectural changes. Third, right-size your context windows — do not deploy models with 128K context windows for use cases that need 4K. Every unnecessary token capacity burns memory at inference time.

Bottom Line

RAMmageddon is real, structural, and not going away on a short timeline. The deliberate reallocation of global semiconductor capacity toward HBM for AI infrastructure — driven by projects like OpenAI’s Stargate consuming 40% of DRAM output — has created a shortage that is now baked into enterprise hardware budgets, PC pricing, and AI deployment costs for the next two to three years. SK Hynix’s planned $10–14 billion U.S. IPO represents the most significant near-term capital commitment toward ending the shortage, but new fab capacity takes 18–36 months to produce shipping product. The practitioners who come out ahead are the ones who lock in supply agreements now, implement software-level memory optimization aggressively, and track the market signals — IPO progress, spot price indices, ASML delivery timelines — that indicate when real relief is coming. Do not wait for prices to normalize. They are not normalizing soon.

0 Comments