SoftBank just took out a $40 billion unsecured loan with a 12-month maturity — and that single structural detail tells you more about OpenAI’s IPO timeline than any press release ever will. Arranged by JPMorgan and Goldman Sachs alongside Mizuho, SMBC, and MUFG, the facility closed on March 27, 2026, days after OpenAI completed the largest private capital raise in technology history. This post breaks down exactly what the loan structure signals, what OpenAI’s financial trajectory looks like heading into a public listing, and how enterprise teams and investors should be positioning right now.

What This Is

The Loan Itself

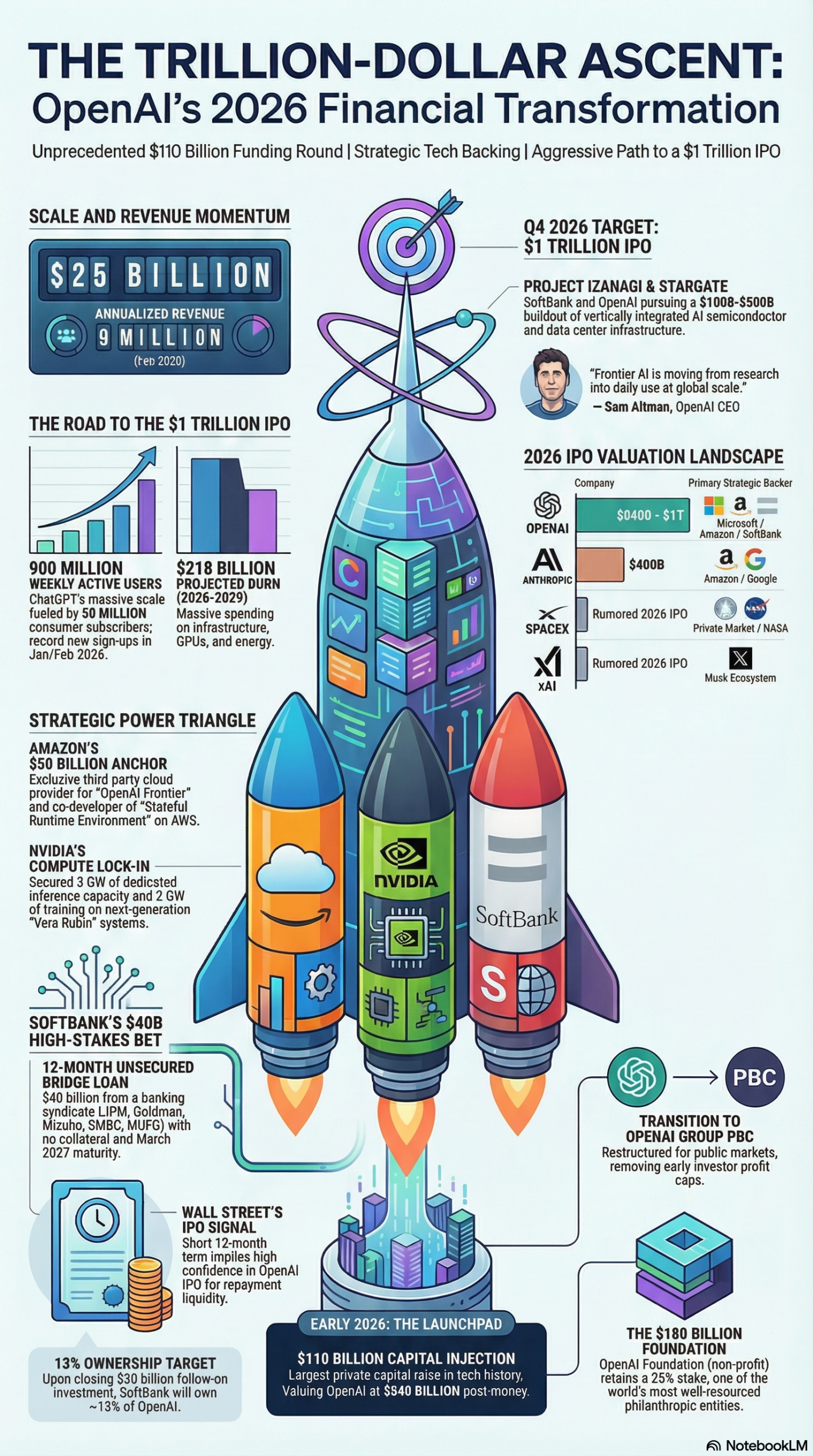

According to TechCrunch, SoftBank secured a $40 billion unsecured bridge loan with a maturity date of March 25, 2027 — exactly 12 months from closing. The lender syndicate reads like a who’s-who of global finance: JPMorgan Chase, Goldman Sachs, Mizuho Bank, Sumitomo Mitsui Banking Corporation (SMBC), and MUFG Bank.

The explicit purpose of the loan is to fund SoftBank’s $30 billion equity commitment to OpenAI’s February 2026 funding round — the largest private capital raise in technology history at $110 billion, per the research report. That round closed at a $730 billion pre-money valuation ($840 billion post-money), nearly triple the size of OpenAI’s own previous record $40 billion raise in 2025.

Two structural details of the loan stand out immediately:

It is unsecured. No collateral was pledged. In conventional lending, this is reserved for borrowers with pristine balance sheets and high lender confidence in near-term liquidity. Pledging no assets on a $40 billion facility signals the banking syndicate believes SoftBank will have the cash to repay — and repay easily — within 12 months.

The maturity is 12 months. Bridge loans are designed to carry a borrower across a gap between now and a known liquidity event. A 12-month maturity expiring in Q1 2027 maps precisely onto the window during which analysts, investors, and the research report project OpenAI’s IPO will occur: Q4 2026 or Q1 2027.

OpenAI’s Corporate Restructuring

Understanding the loan requires understanding what OpenAI has done to its corporate structure. In late 2025, OpenAI converted its for-profit arm into OpenAI Group PBC — a Public Benefit Corporation. This structure preserves a legal mandate around AI safety while removing the profit caps that previously constrained investor returns, per the research report. Removing those caps is a prerequisite for listing on a public exchange. The original non-profit entity now operates as the OpenAI Foundation, retaining a 26% equity stake in the for-profit company — a stake valued at over $180 billion at current valuation, making it one of the wealthiest philanthropic organizations in the world.

SoftBank’s “Total Offense” Posture

SoftBank CEO Masayoshi Son has explicitly framed 2026 as a “total offense” moment for the conglomerate. Beyond the $30 billion equity stake via Vision Fund 2, SoftBank holds a roughly 90% stake in Arm Holdings, which is positioned as a hardware supplier for OpenAI’s next-generation specialized AI chips. The research report notes that OpenAI is expected to become a primary customer for Arm’s AI silicon, creating a vertically integrated stack that ties SoftBank’s software bet directly to its semiconductor holdings.

Why It Matters

For Enterprise Decision-Makers

OpenAI is no longer a vendor you evaluate quarterly. It is becoming infrastructure — the same category as AWS or Azure. The research report documents that AWS is now the exclusive third-party cloud distribution provider for OpenAI Frontier, OpenAI’s enterprise platform for managing teams of AI agents. OpenAI and Amazon are co-developing a Stateful Runtime Environment that lets models retain context and access identity and compute resources through Amazon Bedrock.

That last piece is significant. Stateful AI means your agents remember prior work across sessions — a critical upgrade for any enterprise running production AI workflows where continuity matters. If you’re building multi-step agentic pipelines today, this architecture is the infrastructure your workflows will run on post-IPO.

The IPO also accelerates standardization pressure. Once OpenAI is a public company, it will face quarterly earnings scrutiny, which drives it toward higher-margin, stable enterprise contracts over consumer subscriptions. Enterprise teams that negotiate agreements now, before a public listing increases OpenAI’s pricing leverage, are working from a stronger position.

For Institutional Investors

The loan structure is the signal. JPMorgan and Goldman Sachs do not arrange $40 billion unsecured facilities without high conviction about the borrower’s near-term liquidity profile. As the research report notes, the 12-month term strongly implies a liquidity event by Q1 2027 at the latest. Investors preparing for what could be a record-breaking listing should note that OpenAI is internally targeting a $1 trillion valuation at its public debut — a 19% premium over the current $840 billion post-money valuation.

For Competitors and the AI Ecosystem

OpenAI’s $110 billion raise sets a capital bar that most model labs cannot clear. Anthropic, currently valued at roughly $400 billion per the research report, is running a capital race for the multi-billion-dollar training runs required to stay at the frontier. The OpenAI–Amazon–Nvidia–SoftBank nexus creates a closed-loop system: SoftBank capital funds the equity, Amazon provides the cloud distribution and custom silicon (Trainium), Nvidia supplies the GPU infrastructure, and Arm provides the AI chip architecture. Replicating this vertical integration from scratch is an enormous barrier to entry.

The Data

OpenAI Financial Snapshot — February/March 2026

The following data is sourced from the research report:

| Metric | Value |

|---|---|

| Annualized Revenue Run Rate | $25 billion |

| Post-Money Valuation (Feb 2026 Round) | $840 billion |

| Target IPO Valuation | $1 trillion |

| Weekly Active Users | 900 million |

| Paying Business Users | 9 million |

| Consumer Subscribers | 50 million |

| Projected 2026 Full-Year Revenue | $30 billion |

| Estimated 2030 Revenue | $280 billion |

| Forecasted Cash Burn (2026–2029) | $218 billion |

| Gross Margin (Current) | ~33% (down from 40%) |

| Compute Commitments Through 2029 | ~$600 billion |

Strategic Investor Breakdown — $110 Billion Round

| Investor | Commitment | Structure |

|---|---|---|

| Amazon | $50 billion | $15B initial + $35B contingent |

| SoftBank | $30 billion | Via Vision Fund 2 |

| Nvidia | $30 billion | Strategic equity |

SoftBank Bridge Loan Syndicate

| Lender | Role |

|---|---|

| JPMorgan Chase | Lead arranger |

| Goldman Sachs | Lead arranger |

| Mizuho Bank | Syndicate member |

| SMBC | Syndicate member |

| MUFG Bank | Syndicate member |

Step-by-Step Tutorial: How to Analyze an AI Company’s IPO Readiness

Reading the SoftBank loan correctly is a skill — the same analytical framework applies to any major AI company heading toward a public listing. Here is a step-by-step process for practitioners evaluating AI IPO readiness, whether you’re an enterprise procurement team, a startup building on top of these platforms, or an investor allocating capital.

Phase 1: Map the Capital Structure

Step 1: Identify the funding round size and valuation anchor.

Start with the most recent primary raise. In OpenAI’s case, that’s the February 2026 $110 billion round at an $840 billion post-money valuation, per the research report. Note who participated — strategic investors (Amazon, Nvidia, SoftBank) versus pure financial investors. Heavy strategic participation signals that the company’s value is increasingly tied to partner ecosystems, not just standalone product revenue.

Step 2: Identify bridge financing and loan structures.

Look for any bridge loans, convertible notes, or credit facilities opened after a major raise. These instruments tell you about timing. An unsecured, 12-month bridge loan like SoftBank’s is almost always tied to a near-term liquidity event. Unsecured means the lenders don’t need hard assets because they expect the borrower to generate liquid value (through an IPO, secondary sale, or major cash inflow) before the note matures. Short maturity (12 months versus typical 3–5 year term loans) further compresses the implied timeline.

Step 3: Check the lender roster.

When JPMorgan and Goldman Sachs co-arrange a facility at this scale, they are effectively underwriting their own future IPO mandate. Both banks have large equity capital markets divisions that compete aggressively for blockbuster listings. Participating in the pre-IPO bridge is a way to deepen the banking relationship and position for the lead underwriter role on the public offering.

Phase 2: Evaluate Corporate Structure for IPO Compatibility

Step 4: Confirm profit cap removal.

The single biggest structural blocker for an OpenAI IPO was its nonprofit governance structure with capped investor returns. The late 2025 conversion to OpenAI Group PBC removed those caps, per the research report. For any AI company, check: Are investor return caps in place? Is there a for-profit entity with standard equity economics? Can shares be freely transferred or listed?

Step 5: Verify non-profit carve-outs and governance.

The OpenAI Foundation retaining a 26% stake in the for-profit entity is a novel structure. Practitioners evaluating governance risk should understand that the Foundation’s ownership creates a permanent strategic anchor. This is a feature (aligned safety mission) and a risk (a large, non-commercially motivated shareholder can vote on major decisions). For enterprises and investors, assess how this governance structure affects long-term pricing and product decisions.

Step 6: Assess management continuity.

Public markets hate leadership uncertainty. Note that Sam Altman’s position as CEO has been solidified following the late 2023 governance crisis. His February 2026 blog post explicitly framing infrastructure scaling as the primary competitive moat, quoted in the research report, represents the kind of clear strategic narrative that IPO roadshows are built around.

Phase 3: Stress-Test the Revenue and Margin Model

Step 7: Calculate the path to positive free cash flow.

OpenAI’s current gross margins have compressed from 40% to approximately 33% as inference spending has accelerated, per the research report. The $218 billion projected cash burn between 2026 and 2029 means the company will not be self-funding its infrastructure buildout from revenue alone. Public market investors will scrutinize: (a) the pace of margin recovery as model efficiency improves, (b) the revenue mix shift toward higher-margin enterprise contracts, and (c) the timeline to positive operating cash flow.

Run this analysis yourself: Take the projected 2030 revenue of $280 billion. Apply a hypothetical 50% gross margin (assuming token costs decline and enterprise mix grows). Subtract estimated operating expenses (R&D, sales, infrastructure). Does the company reach free cash flow breakeven before its debt maturities come due? For OpenAI at current trajectory, the answer is yes — but only if inference costs continue declining at the pace driven by models like o3 and o4.

Step 8: Evaluate the user growth quality.

900 million weekly active users sounds extraordinary. But the more actionable number for IPO analysis is the 9 million paying business users generating enterprise-grade revenue. Consumer free users (ad-supported or freemium) carry low monetization multiples; enterprise SaaS contracts carry 8–12x revenue multiples. Track the ratio of enterprise to consumer revenue, and watch for announcements of minimum annual contract values in enterprise deals.

Step 9: Map infrastructure commitments against revenue projections.

OpenAI’s compute commitments through end-of-decade are estimated at $600 billion, with Stargate Project aspirations of up to $500 billion in U.S. AI infrastructure, per the research report. The secured infrastructure — including 3 GW of dedicated inference capacity and 2 GW of training on Nvidia’s Vera Rubin systems — must be matched against revenue growth. If revenue scales faster than compute costs, margins recover. If compute costs grow faster than revenue, the cash burn extends. For practitioners, monitoring Nvidia earnings calls and OpenAI’s quarterly API pricing is a real-time proxy for this ratio.

Phase 4: Monitor IPO Timing Indicators

Step 10: Watch for SEC S-1 filing.

The formal IPO process begins with an S-1 registration filing with the Securities and Exchange Commission. For a company the size of OpenAI, expect a confidential filing first (allowing the company to negotiate with regulators and address comments before public disclosure), followed by a public S-1 six to twelve weeks before the pricing date. With the SoftBank loan maturing March 25, 2027, and an internal target of Q4 2026 for the IPO per market analysis in the research report, watch for a confidential S-1 filing as early as Q2 or Q3 2026.

Step 11: Track banker appointment announcements.

Before an IPO, companies formally appoint lead underwriters (book-running managers). Given JPMorgan and Goldman Sachs’s participation in the SoftBank bridge loan, both banks are heavily favored to lead the OpenAI offering. A formal appointment announcement is typically made three to six months before the IPO. Watch for this signal.

Step 12: Monitor secondary market pricing.

OpenAI shares trade on private secondary markets (platforms like Forge Global and Caplight). As IPO timing becomes more certain, secondary pricing typically converges toward the expected IPO price. A sustained secondary market valuation above $900 billion would signal strong institutional appetite at the $1 trillion public target.

Expected Outcomes

If you apply this framework consistently, you should be able to determine — within a 90-day window — when a major AI company like OpenAI is within six months of a public listing. The SoftBank loan structure, read correctly, places OpenAI’s IPO window between Q3 2026 and Q1 2027 with high confidence.

Real-World Use Cases

Use Case 1: Enterprise Procurement Timing

Scenario: A Fortune 500 head of technology strategy is deciding whether to sign a three-year enterprise agreement with OpenAI now or wait until after the IPO.

Implementation: Apply the analysis framework above. Pre-IPO, OpenAI has strong incentives to lock in large enterprise contracts to demonstrate revenue quality on the S-1 filing. This creates negotiating leverage for buyers — you can extract better pricing, SLAs, and custom model access in exchange for multi-year commitments. Post-IPO, OpenAI faces quarterly earnings pressure and will have less flexibility to offer bespoke pricing.

Expected Outcome: Enterprise teams that negotiate agreements in Q2–Q3 2026 are likely to secure materially better pricing and terms than those that wait until after the listing. The window closes when the S-1 is filed publicly.

Use Case 2: AI Infrastructure Vendor Assessment

Scenario: A cloud engineering team is evaluating whether to build their agentic AI infrastructure on OpenAI’s stack via AWS, or diversify across multiple model providers.

Implementation: Review the AWS–OpenAI partnership details from the research report: AWS is the exclusive third-party cloud distribution channel for OpenAI Frontier, and the two companies are co-developing a Stateful Runtime Environment via Amazon Bedrock. This means OpenAI’s enterprise-grade agentic capabilities will be deeply integrated with AWS infrastructure — not available at equivalent depth on Azure or GCP.

Expected Outcome: Teams already on AWS have a strong path-of-least-resistance to adopt OpenAI’s most advanced agentic features. Teams on other clouds should factor in the integration depth gap when modeling total cost of ownership and time-to-production for complex agentic workflows.

Use Case 3: Competitor Intelligence for AI Startups

Scenario: A startup building on top of open-source or alternative frontier models (Anthropic Claude, Google Gemini) wants to understand how the OpenAI capital raise changes their competitive landscape.

Implementation: Use the capital structure analysis to quantify the moat. OpenAI now has $600 billion in secured compute commitments and access to Nvidia’s most advanced Vera Rubin systems — 3 GW of inference, 2 GW of training. This hardware advantage translates directly into model capability: larger training runs, faster iteration, lower inference latency at scale. Anthropic, valued at ~$400 billion per the research report, is capital-constrained by comparison.

Expected Outcome: Startups relying on cost arbitrage (using cheaper models than OpenAI) have a viable window of 12–18 months before OpenAI’s efficiency improvements narrow that gap. Those building differentiated workflows or vertical-specific fine-tuned models have longer runway. Use this analysis to set your product roadmap priorities.

Use Case 4: Investment Portfolio Positioning

Scenario: An institutional fund manager is assessing how to position around the anticipated OpenAI IPO.

Implementation: Monitor the 12 indicators outlined in the Step-by-Step Tutorial above. Focus especially on secondary market pricing convergence and formal underwriter appointments. Given the $1 trillion target IPO valuation versus the $840 billion post-money private valuation, the implied uplift is approximately 19%. Historical data from major tech IPOs (Facebook, Google, Snowflake) suggests that “hypergrowth” AI listings at this scale can trade significantly above or below the initial pricing depending on market conditions at listing time. The $218 billion projected cash burn through 2029 will be the primary bear case on the IPO roadshow.

Expected Outcome: Investors who complete pre-IPO due diligence and establish conviction on the cash flow timeline will be positioned to act quickly at listing. The window between S-1 filing and pricing is typically only a few weeks for high-demand listings.

Use Case 5: Content and Marketing Teams Evaluating AI Tool Lock-In

Scenario: A marketing agency managing AI-powered content workflows wants to understand the risk of over-reliance on OpenAI tools as the company approaches a public listing.

Implementation: Assess your current workflow dependencies: How many of your production pipelines call the OpenAI API directly? Are you using GPT models via OpenAI directly, or through Azure OpenAI? Post-IPO pricing pressure is real — public companies optimize for margin. Evaluate where you can introduce model-agnostic abstraction layers (LangChain, LlamaIndex, or custom routing logic) that let you swap underlying models without rewriting application logic.

Expected Outcome: Teams with model-agnostic architectures maintain pricing leverage. Teams hard-coded to OpenAI API endpoints face renegotiation risk every contract cycle. Build the abstraction layer now, while migration costs are low.

Common Pitfalls

Pitfall 1: Confusing Bridge Loan Purpose with Revenue Signal

The $40 billion loan is not evidence that OpenAI is cash-flow positive or that SoftBank needs emergency liquidity. It is a bridge instrument — designed to fund the equity commitment while SoftBank manages its overall balance sheet. Analysts who misread it as distress financing are wrong. It is, per the research report, a signal of lender confidence in near-term IPO proceeds, not a sign of financial weakness.

Pitfall 2: Over-Weighting the Headline Valuation

$840 billion post-money sounds staggering. But remember: the company projects $218 billion in cash burn through 2029 and current gross margins of ~33%, down from 40%. Headline valuation without a coherent path to positive free cash flow is a risk, not a guarantee. Public market investors will price this differently than the strategic investors who participated in the private round with platform-lock-in motivations.

Pitfall 3: Ignoring Governance Risk from the Foundation’s 26% Stake

The OpenAI Foundation’s 26% equity stake — valued at over $180 billion — gives it significant voting power in major decisions. Enterprises and investors who assume standard public-company governance post-IPO should read the prospectus carefully. The Foundation’s mission-driven priorities may not always align with shareholder return maximization. This is not necessarily negative, but it is different, and markets will need time to price it accurately.

Pitfall 4: Assuming the IPO Window Is Fixed

The SoftBank loan matures March 25, 2027. If market conditions deteriorate between now and then — a major AI safety incident, regulatory action, or a significant equity market correction — the IPO could be delayed beyond Q1 2027. SoftBank could roll the loan or find alternative liquidity. Do not treat the 12-month maturity as a hard deadline for the IPO; treat it as a high-confidence probabilistic indicator.

Pitfall 5: Underestimating Inference Cost Decline as a Margin Driver

Many analysts focus on the $218 billion cash burn without adequately modeling inference cost deflation. OpenAI’s own efficiency improvements — and competition from open-source models — have driven token costs down dramatically year over year. If this trend continues, gross margins can recover to 50%+ even without changing the revenue mix. The path to IPO profitability runs directly through token cost curves, not just revenue growth.

Expert Tips

Tip 1: Track the Arm AI chip roadmap alongside OpenAI news.

SoftBank’s integration play depends on Arm-designed AI chips becoming OpenAI’s preferred inference silicon. Watch Arm’s developer ecosystem announcements and OpenAI’s hardware partnership news together — they are part of the same strategy as documented in the research report.

Tip 2: Use secondary market pricing as a real-time IPO temperature gauge.

Private secondary markets for OpenAI shares (Forge Global, Caplight) price continuously based on institutional demand. A sustained climb toward $900 billion+ secondary valuation in Q2–Q3 2026 would be a leading indicator of IPO confidence. Set up alerts for secondary market data providers.

Tip 3: Read the AWS SEC exhibit, not just the press release.

The research report cites an official SEC exhibit from the Amazon-OpenAI partnership announcement. SEC filings contain exact contractual language around exclusivity, minimum commitments, and termination rights — the details that determine how locked-in OpenAI actually is to AWS infrastructure and vice versa.

Tip 4: Price your enterprise AI contracts against the S-1 filing date.

Once OpenAI’s S-1 is public, the company’s cost structure, margins, and revenue per user become public knowledge. Enterprises with existing contracts can benchmark their own economics against the disclosed figures. Start building the internal analysis framework now so you can act quickly when the S-1 drops.

Tip 5: Model the SoftBank LTV risk as a tail scenario.

The research report notes that SoftBank’s loan-to-value (LTV) ratio may temporarily breach its 25% ceiling. If OpenAI’s private valuation were marked down significantly before the IPO, SoftBank could face margin calls or forced asset sales (including its Arm stake). This tail scenario would have cascading effects on the entire OpenAI capital structure. Low probability, but worth stress-testing in any position sizing model.

FAQ

Q1: Why is the loan unsecured? Doesn’t that increase lender risk?

In a standard lending context, yes. But at this scale and with this syndicate, the banks are making a judgment that SoftBank’s overall balance sheet — including its ~90% stake in Arm Holdings (a publicly traded company) and its $30 billion equity position in OpenAI — provides more than adequate implicit coverage. The lack of formal collateral is a term of convenience for SoftBank, not an oversight by the lenders. It signals extremely high confidence in the borrower’s near-term liquidity, per the research report.

Q2: What happens if the OpenAI IPO is delayed past March 2027?

SoftBank would need to either repay the $40 billion from other liquidity sources, roll the loan (negotiate a new maturity with the syndicate), or sell other assets to cover the obligation. SoftBank has done all three in prior cycles. The more consequential risk is reputational: a missed repayment would signal that the IPO thesis was wrong, which could pressure OpenAI’s private valuation and complicate the eventual listing.

Q3: Does the IPO change OpenAI’s product strategy for enterprise customers?

Almost certainly yes, in one specific direction: public companies maximize margin, and enterprise software has higher margins than consumer subscriptions. Post-IPO, expect OpenAI to invest more heavily in enterprise sales, compliance features (SOC 2, HIPAA, FedRAMP), and dedicated customer success — while consumer pricing remains competitive to protect the 900 million WAU base that drives brand and data flywheel value, per the research report.

Q4: How does the OpenAI Foundation’s 26% stake affect the IPO price?

The Foundation’s stake creates a governance overhang that IPO investors will want priced in. On the positive side, it signals mission alignment and reduces the risk of purely short-term commercial decisions. On the negative side, a 26% non-commercial shareholder with a safety mandate can complicate aggressive product expansion decisions. Public market precedent for this governance structure is limited — investors will look at Alphabet’s dual-class share structure and Benefit Corporation rules for comparison. Expect the S-1 to dedicate extensive legal disclosure to the Foundation’s rights and limitations.

Q5: Is the $1 trillion IPO valuation target achievable?

At $30 billion projected 2026 revenue and a $1 trillion target valuation, the implied price-to-sales multiple is approximately 33x. That is aggressive by traditional software standards but not unprecedented for AI infrastructure companies with network effects and platform lock-in. Snowflake debuted at roughly 100x forward revenue in 2020. Microsoft trades at 12x forward revenue today. OpenAI’s actual IPO multiple will depend heavily on gross margin trajectory, cash burn visibility, and market sentiment toward AI at listing time. The research report notes analysts are shifting valuation frameworks from SaaS multiples toward infrastructure and operating system comparables — a framing that supports higher multiples.

Bottom Line

SoftBank’s $40 billion unsecured bridge loan, arranged by JPMorgan and Goldman Sachs with a 12-month maturity expiring March 2027, is the clearest structural signal yet that OpenAI will IPO by Q4 2026 or Q1 2027. With $25 billion in annualized revenue, 900 million weekly active users, and a $840 billion post-money valuation from the largest private capital raise in technology history, OpenAI is entering the public markets from a position of extraordinary scale — but also extraordinary cash burn, with $218 billion projected through 2029. The practitioner play is to act before the S-1 drops: negotiate enterprise contracts while OpenAI needs your revenue metrics for the prospectus, build model-agnostic AI architectures to preserve pricing leverage, and stress-test your infrastructure dependencies on the AWS-OpenAI-Nvidia stack. The window between now and a confirmed S-1 filing is likely measured in months, not years.

0 Comments